SOUTH AFRICA: inflation control

- Jul 27

- 1 min read

South Africa is the smallest G20 economy at market exchange rates.

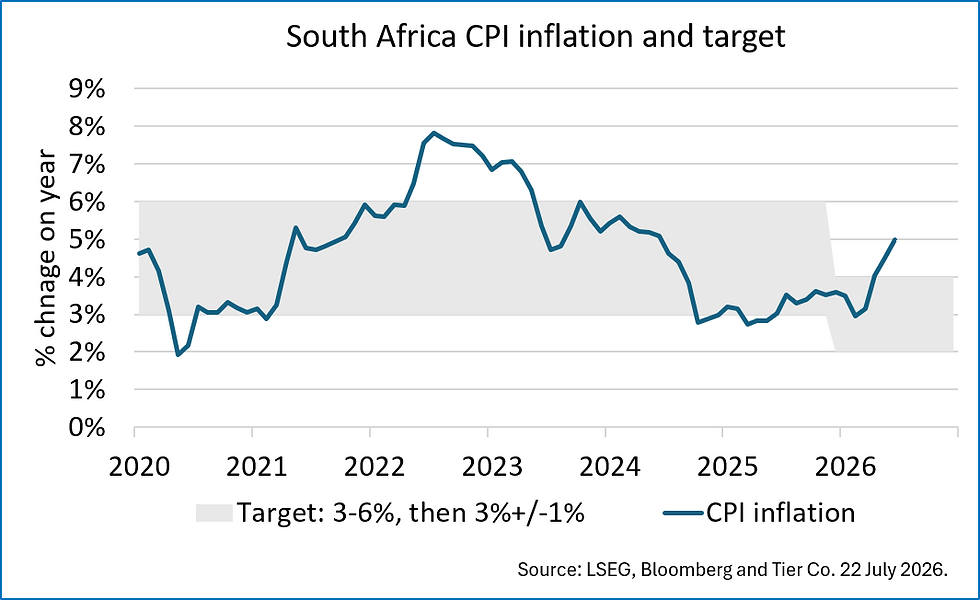

The population is expected to continue to grow in coming years, with the proportion of 16-64 year olds remaining relatively stable. Potential GDP growth we estimate at around 1.6% p.a. Growth in 2025 was a little below that, at 1.1%. That is one reason why inflationary pressures were relatively subdued, with CPI inflation at the bottom of its old 3-6% target range. The announcement of the new target in December 2025 (the old target had been in place for 25 years) was welcomed in financial markets with the rand strengthening and long-term bond yields falling. However, data to June 2026 show the inflation rate rising to 5.0%, and underling inflation also increasing - to 4.1%.

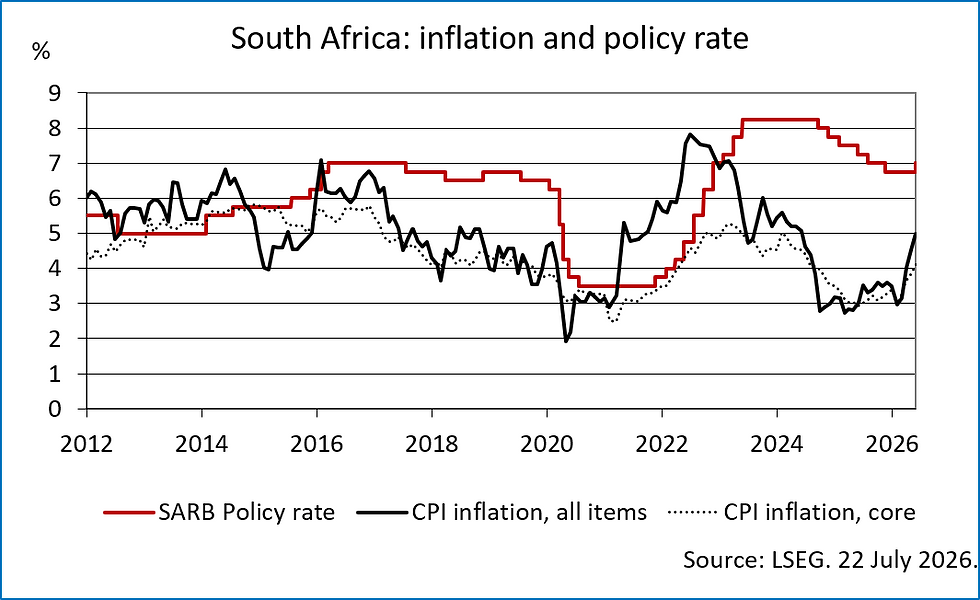

Broad money growth is broadly in line with expected nominal GDP growth and the amount of credit to the private non-financial sector, at 67% of GDP, is well contained. These trends, and the fact that the policy rate is already at 7%, suggest that any inflation increase will be relatively short-lived.

The government’s debt level, however, is expected to trend higher over the next five years. South Africa’s small current account deficit and positive net foreign assets mean the external position is pretty resilient.

The main weak spot is that South Africa still ranks pretty low on corruption perceptions and, indeed, many governance metrics.